Another Good Year For Equity Markets

Jan 24, 2014

For a year that started off with concerns about another euro crisis and a triple dip recession in the UK, developed equity markets performed strongly in 2013.

Index | 2013 Change |

FTSE 100 | +14.4 |

FTSE All-Share | +16.7 |

Dow Jones Industrial | +26.5 |

Standard & Poor’s 500 | +29.6 |

Nikkei 225 | +56.7 |

Euro Stoxx 50 | +17.1 |

Hang Seng | + 2.9 |

MSCI Emerging Markets (£) | - 6.7 |

The performances shown above hide several factors which could be important in 2014:

- Another poor year for the commodity-based multinationals was one major reason why the UK stock market failed to keep pace with the US. There is little expectation of a commodities rebound in 2014.

- The more UK-centric businesses again did much better, witness the performance of the FTSE 250, which measures the 250 companies below the top 100 – about 15% of the UK stockmarket. The FTSE 250 gained 28.8% in 2013, which explains why the broader FTSE All-Share Index repeated its 2012 out-performance of the more widely quoted FTSE 100.

- Sterling had a good year, which reduced the returns for UK investors in many foreign markets. This was very noticeable in Japan, where sterling rose by 24.9% against the Yen. Even against the dollar the pound added 1.9%. There is now some concern that the strength of sterling will start to hit UK exports.

- Emerging markets had a generally disappointing year, witness the fall in the MSCI index. The US Federal Reserve’s plan for tapering QE (see below) worried investors in emerging markets, particularly those which rely on foreign capital inflows.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

Is 8% Enough?

Nov 8, 2013

The final level of contributions under pension auto-enrolment is probably too low, according to one leading pensions organisation.

Last month marked the first anniversary of pension auto-enrolment, which is gradually being rolled out across the UK employed workforce, starting with the largest employers. So far take up has been better than many had predicted, with less than 1 in 10 employees opting out after auto-enrolment, according to the DWP.

The low opt out rate probably reflects the efforts which have put into the process by the major employers – like the supermarkets and banks. However, another factor could well be the current level of contributions: the minimum total contribution (employer and employee) in 2013/14 is 2% of band earnings (annual earnings between £5,668 and £41,450). If the employer pays just their required 1%, the most an employee’s outlay will be is £23.85 a month after basic rate tax relief.

Total contributions are set to rise to 5% (2% employer minimum) in October 2017 and 8% (3% employer minimum) a year later. Thus, if an employer limits contributions to the legal floor, in five years’ time their employees’ contributions would be five times the current level.

Whether that will prompt a rise in opt out rates remains to be seen, but there are already voices saying the 8% total is not enough. The latest is the Pensions Policy Institute (PPI), which has used a statistical model developed by King’s College, London to look at the chances that the combination of auto-enrolment and the forthcoming single tier state pension will provide an adequate retirement income. Its main conclusion was that for a median earner, a contribution of 8% of band earnings throughout their working life will give them “less than fifty-fifty chance of achieving an adequate retirement income.”

The PPI’s research echoed the findings of DWP work in the same area of retirement income adequacy. In particular the PPI said that higher earners need to contribute more than median and low earners because the proportion of their final earnings presented by the single-tier pension is that much less. Their calculations are shown in the chart below.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

ISA Freeze?

Nov 6, 2013

The Treasury has been talking about an ISA cap.

The Treasury has been consulting with financial services companies about the possibility of a cap on the amount that can be held in ISAs according to reports in one national newspaper. A figure of £100,000 was allegedly suggested by one Treasury official. There have been no denials from the Treasury, which has said it was just listening, not putting forward any firm proposals.

The idea of putting a cap on ISA investment is not new. When ISAs were first proposed as a replacement for PEPs (Personal Equity Plans) back in the late 1990s, there were suggestions that a combined ISA/PEP ceiling of £50,000 should be introduced. The outcry which followed prompted the Chancellor of the time, Gordon Brown, to back down. The return of a cap consideration now is unsurprising, given the value of ISA funds had reached £443bn by the start of this tax year and the annual income tax cost to the Exchequer is put at £1.75bn. That cost could increase significantly when interest rates start to rise.

With pension allowances being cut again from next April, ISAs could be the next savings vehicle to which the Treasury takes the axe. There are some ISA millionaires, reportedly a concern for the Treasury, but the numbers are almost certainly very small: if you had invested the maximum in PEPs and ISA from January 1987, your total contributions would amount to £212,320 and you would have needed an annual return of nearly 12% after all charges to hit a seven figure value now. The £100,000 target is clearly much easier and one estimate is that it would catch around 2% of all ISA investors.

Will it happen? If anything, an ISA cap looks more like an immediate post-election move rather than something that will happen soon. Nevertheless, as Mr Osborne has announced that he will be presenting the Autumn Statement on December 4, you might want to think about making this year’s ISA contribution in November rather than waiting for next March.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

Labour Party Tax Policy

Oct 4, 2013

Not much wiser

Last month’s Labour Party conference produced little in the way of fresh tax policy details. Ed Balls, the Shadow Chancellor, said little new and neither did his Shadow Treasury chief secretary, Rachel Reeves. So what do we know so far?

- The 10p income tax band will be reintroduced, having been culled by Gordon Brown shortly before he became prime minister.

- There will be a mansion tax for properties worth more than £2m, echoing Liberal Democrat proposals.

- The final planned reduction in corporation tax from 21% to 20% in 2015 will be scrapped, with the money raised being used to cut business rates for small businesses.

- “The highest earners” will have the tax relief on their pension contributions cut to basic rate, probably using a method legislated for in 2010, but then abandoned as too complex.

- The top rate of tax will return to 50% at an income level of £150,000.

The biggest piece of news from the conference was not on the tax front, but Ed Miliband’s promise of a 20 month freeze on utility prices to the start of 2017. This pledge served as a sharp reminder that utility company shares, long popular among income-seeking investors, are not without political risk.

The Financial Conduct Authority does not regulate tax advice.

How much income will you need in retirement

Oct 4, 2013

The Department for Work and Pensions (DWP) has been mulling over the answer to this question

The gradual introduction of pension auto enrolment and the forthcoming reworking of the state pension system will alter the pension landscape in the years ahead. The DWP has been considering how it should gauge the impact of its measures on retirement incomes, something that you might have thought deserved attention a little earlier on in the reform process. The Department’s number crunchers have produced estimates of adequate retirement incomes as a proportion of pre-retirement incomes. The results are shown in the table below.

Pre-retirement Earnings Band | Replacement Rate % |

Less than £12,200 | 80 |

£12,200 - £22,400 | 70 |

£24,400 - £32,000 | 67 |

£32,000 - £51,300 | 60 |

Over £51,300 | 50 |

If the earnings bands look rather strange, it is because the DWP has taken a short cut in deriving the table. Instead of starting from scratch, it just copied the income replacement rate table produced by the Pensions Commission in 2004 and updated it in line with the growth in earnings. The average increase in each band of around 28% is less than price inflation since 2004, based on the RPI, but just about matches CPI.

The DWP calculates that on the basis of its proposed replacement rates, 12.2 million people are still facing inadequate retirement incomes, even after its reforms kick in. It says that “Roughly half of these [12.2m] are within 20% of their target amount, with the remainder facing a more significant challenge. This is a particular issue for moderate and higher earners.”

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Base Rate at 0.5% until 2016!

Sep 13, 2013

August was not a quiet month at the Bank of England.

The new Governor of the Bank of England, Mark Carney, came to the job with a ‘rock star’ central banker reputation which his predecessor, Sir Mervyn King, lacked. Mr Carney was expected to reform the Bank’s policies and in August he took a major step in this direction.

What he did was make an announcement which fits the economic euphemism of the moment, ‘forward guidance’. At its simplest, forward guidance means telling the market the central bank’s views of (and plans for) future short term interest rates. However, in the UK context it was not that simple. Mr Carney told us that the Bank “intends not to raise Bank Rate from its current level of 0.5% at least until … the unemployment rate has fallen to a threshold of 7%”, which the Bank’s economists predict will be in mid- 2016. The current (April-June) unemployment figure is 7.8%.

It was not – despite the various “another three years” headlines – a blanket promise. The Bank detailed three “knockouts” (its words) that would prompt earlier action:

1. The Bank considers it more likely than not, that CPI inflation 18-24 months ahead will be 2.5% or more;

2. Medium-term inflation expectations no longer remain “sufficiently well anchored”; and

3. A significant threat to financial stability related to the continued low rates.

The Bank (and the Chancellor’s) hope is that the guidance encourages companies and consumers to borrow, safe in the knowledge they will not be hit by a sudden rise in rates. Mr Carney used a similar approach in his last job, at the Bank of Canada, when he said in April 2009 rates would stay flat for at least a year.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

NOT-SO-PREMIUM BOND

Aug 16, 2013

National Savings & Investments are cutting the prize money on premium bonds.

In June, National Savings & Investments (NS&I) announced reductions of between 0.4% and 0.5% from 12 September on three of its variable rate offerings, the most significant being a cut in the Income Bond rate from 1.75% to 1.25%. At the time, some of the press coverage commented that the move increased the relative appeal of premium bonds, where the underlying prize money equated to 1.5% tax-free interest.

Last month NS&I reacted to the resultant inflows into premium bonds by cutting the prize money rate to 1.3% from 1 August. The lower rate will result in two changes:

- The chances of any one bond winning a prize in the monthly draw will fall from 1:24,000 to 1:26,000.

- The distribution of winnings will alter (see chart), with an even higher proportion (98.1%) of successful bonds earning their owners the minimum prize of £25.

1.3% tax-free doesn’t look bad if you are a higher rate taxpayer – you would have to earn 2.17% gross interest to match it, which beats any instant access account currently available. However, the 1.3% is theoretical and what you would actually earn depends upon lady luck. The statisticians say that the skew of prizes and the minimum of £25 means on average you will earn less than 1.3%.

Value of prize | Number of prizes in July 2013 | Number of prizes in August 2013 (estimate) |

£1,000,000 | 1 | 1 |

£100,000 | 5 | 3 |

£50,000 | 9 | 6 |

£25,000 | 20 | 11 |

£10,000 | 49 | 30 |

£5,000 | 97 | 58 |

£1,000 | 1,142 | 789 |

£500 | 3,426 | 2,367 |

£100 | 33,552 | 11,891 |

£50 | 33,552 | 11,891 |

£25 | 1,831,461 | 1,724,014 |

TOTAL | 1,903,314 | 1,751,061 |

P.S. If you are thinking of that £1 million jackpot, then don’t plan your retirement around it: the odds of winning the top prize in the monthly draw are now less than 1 in 45,500,000,000.

Pension Tax Relief

Aug 9, 2013

Fancy a 30% flat tax relief on your pension contributions?

In 2006 the previous government introduced what it described as ‘pension simplification’, a radical reworking of the pension tax rules. Ever since, there has been a process which has now gained the label of ‘complification’ – adding complexity back into the pension tax system. The current government can take a fair slice of the blame, with its efforts to cut back the cost of tax relief by twice reducing both the lifetime allowance (on total benefits) and the annual allowance (on contributions).

A recent paper from the Pension Policy Institute (PPI) examined who benefits from the current pension regime and highlighted two tax points:

- Basic rate taxpayers are estimated to make 50% of the total pension contributions, but benefit from only 30% of pension tax relief. In contrast, 50% of all pension tax relief goes to higher rate taxpayers, with the balance going to additional rate taxpayers, while these groups make 40% and 10% of the total contributions respectively.

- Currently 77% of pension lump sums by number are under £40,000, but these account for just under a quarter of the tax relief on lump sums. At the opposite end of the scale 2% of lump sums are worth £150,000 or more and they attract nearly a third of tax relief on lump sums.

The PPI’s concluded that instead of marginal rate income tax relief, a flat rate relief of 30% for everyone would be better at incentivising low and middle income earners and spreading the benefit of tax relief more evenly. It looked at a number of options for cutting back on the lump sum, but concluded that these would have limited immediate effect because any change could not be made retrospectively.

The PPI’s ideas on flat rate relief should not be dismissed as just the musings of another think tank. They echo proposals from the Centre for Policy Studies, a think tank founded by Sir Keith Joseph and closely linked to the Conservatives. The other main political parties have both talked about cutting tax relief for high earners, so the writing may well be on the post-election wall.

The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.

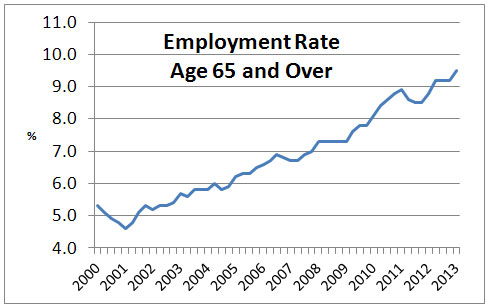

When I'm 64+...

Aug 2, 2013

The number of people aged over 65 in work has reached a new record.

There are now over one million people in work aged 65 or over according to the latest statistics from the ONS. That represents nearly one in ten of the 65 and older population – more than double the proportion at the start of 2001. As the graph shows, there has been a steadily rising trend, seemingly immune to the vagaries of the UK economy since the turn of the millennium.

ONS attributes the breaching of the one million threshold to more people staying on in work and also more people of this age group in the population (the first tranche of the post-war baby boomers is now 65+). The abolition of 65 as a statutory retirement age, which took full effect in October 2011, has probably also helped boost the in-work numbers.

ONS does not define the proportion of the 65+ workers whosefinancial situation meansthat they have no alternative to continued employment, even if it is generally part time. The generation now retiring is often thought of as the lucky ones because their working life coincided with the era of final salary pensions, but that is something of an oversimplification. Final salary schemes were not the province of small employers, nor were those in self-employment able to benefit.

If the idea of working beyond 65 does not appeal to you, make sure your retirement provision is adequate. Otherwise, B&Q may beckon…

What you think happens now, might eventually happen in future.

Jul 5, 2013

The Government is consulting on reforms to intestacy.

What happens if you die leaving only your spouse/civil partner, no children and no will?

You might imagine that everything goes to your spouse or partner, but currently that is not always the case. Under the intestacy rules for England and Wales, a surviving spouse/civil partner would receive:

- Personal chattels

- £450,000 outright; and

- One of half the residue of the estate outright.

The other half of the residue would go to your parent(s) or, if your parents are no longer alive, your siblings. (If your siblings, too, have predeceased you, it goes to their children.) The rules in Northern Ireland are very similar, while Scotland has its own distinctly Scottish regime.

The Ministry of Justice is now proposing to reform English and Welsh intestacy rules, so that where there are no children, the surviving spouse will inherit the whole estate. There are also revisions planned for the estate distribution when there are children involved.

The ministry says that its proposed changes will “ensure the laws on intestacy become closer aligned with public expectations.” However, any reform will not alter the fact that an up to date will that spells out what you want is a better course of action than relying on the state’s interpretation through the intestacy rules.

Your will is up to date, isn’t it..?

The Financial Conduct Authority (FCA) does not regulate will writing or estate planning. |