NEXT YEAR’S PENSION REFORMS

Aug 7, 2014

~~The Government has set out further thoughts on what pensions will look like from next April.

The Chancellor’s Budget bombshell of pension reform was accompanied by a consultation document setting out his broad proposals for industry comment. The consultation period ended in early June and in mid-July the Government issued its response. There were few surprises, but some tweaks of note:

• As expected, there will be measures to prevent the new flexibility being used to prove tax-efficient remuneration. Broadly speaking, if you draw more than the tax-free lump sum from your defined contribution pension scheme, your scope for further contributions to such schemes will fall from £40,000 per tax year to £10,000.

• The Government has abandoned the idea of outlawing transfers from private sector defined benefit schemes (e.g. final salary schemes) to defined contribution arrangements. However, it will require anyone wishing to undertake such a transfer to first obtain professional advice. Transfers from public sector defined benefit schemes will not be possible unless the scheme is funded – a rarity outside local Government.

• Guidance – not independent advice – will have to be offered when benefits are drawn. The Treasury will initially design and implement this, with guidance primarily coming from two existing bodies, the Pensions Advisory Service and the Money Advice Service. Product providers will not be involved in supplying the guidance, but they will have to meet part of its cost. Concerns remain about how effective this will be given the short timescale and potential demand.

• The minimum age for drawing benefits will generally rise to 57 in 2028, with further increases thereafter in line with state pension age thereafter, maintaining a gap of 10 years.

• The 55% tax charge on drawdown funds payable on death will change, but the Government coyly says “any changes have the potential for unforeseen and unintended consequences” and so deferred announcing its decision until the Autumn Statement, which probably means early December.

A still clearer outline of the changes should emerge this month as the Government has promised draft legislation for technical consultation.

For ISA Read NISA

Jul 4, 2014

1 July 2014 marked the end of ISAs and the beginning of NISAs.

It was less than four months ago that George Osborne announced that ISAs would be replaced with ‘New ISAs’ (NISAs).

The news was overshadowed by the pensions reforms, so as a reminder, here is what the rules are now:

• All ISAs became NISAs on 1 July 2014.

• The maximum contribution into a NISA is £15,000 in 2014/15. This is reduced by any amount you have already invested in ISAs in the current tax year.

• The full £15,000 can be invested in a cash NISA or a stocks and shares NISA, or you can mix and match between the two. You will still be able to arrange two separate NISAs – a cash NISA and a stocks & shares NISA.

• The £15,000 limit also applies to cash NISAs for 16 and 17 year olds (who can also have a £4,000 Junior ISA).

• Interest on cash held in a stocks & shares NISA is now tax free, whereas before it was subject to a flat 20% charge.

• It is now possible to switch from the stocks & shares component to the cash component. A move in the opposite direction has long been possible, but until 1 July it was a one-way trip. Now you may switch between them.

• Investment rules for stocks & shares NISAs have been slightly relaxed in the wake of the changes to the cash interest rules. For example, retail bonds with terms of less than five years can now be held in a stocks & shares NISA.

These changes will mean new product developments, with some providers planning to incorporate both cash and stocks & shares components within a single NISA.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. Tax laws can change.

THE PENSIONS ACT 2014

Jun 11, 2014

The new state pension regime moved a step closer in May.

On 15 May the Pensions Bill 2013 finally became the Pensions Act 2014 after more than a year working its way through parliament. It is a major piece of legislation, which will ultimately create widespread change to the pension landscape. The main areas the Act covers are:

• Single tier pension The Act legislates for the introduction of the new single tier state pension from April 2016. The Department for Work and Pensions (DWP) says that this is worth £148.40 a week in 2014/15 terms, although transitional rules mean that few people will initially receive this amount.

• State pension age The Act increases the state pension age (SPA) to 67 by April 2028. It also provides the framework for regular reviews of the SPA based on changes to life expectancy.

• Bereavement support payments From 2016/17, the complex existing bereavement payments system will be replaced by a single lump sum, plus tax-free monthly payments lasting for one year only. The widowed parent’s allowance, payable until a child ceases to be eligible for child benefit and currently worth £111.20 a week, will disappear for new claimants, bringing a long term reduction in government expenditure.

• Private pensions The Act introduces a range of changes to private pensions, many of which will not take effect immediately. These include provisions to allow for automatic transfer of small pension pots, a ban on refunds of pension contributions to short term employees, and powers to cap charges for certain pension schemes.

The Pensions Act 2014, together with forthcoming reforms to how retirement benefits can be drawn, mark a generational overhaul in pension rules. Whatever retirement plans you have, they will almost certainly need to be reviewed.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. The value of tax reliefs depends on your individual circumstances. Tax laws can change.

STUDENT LOANS: REPAYMENT BECOMES WRITE OFF

Jun 10, 2014

~~New research suggests that it may not make financial sense to pay off student loans early.

The higher education funding system in England for studentschanged dramatically in 2012/13, with the most notable reform a near tripling of the maximum tuition fee (and corresponding fee loan) from £3,375 to £9,000. The terms for loan repayment were also changed:

• The rate of interest rose from RPI to between RPI and RPI+3%, depending upon student income.

• The threshold income at which repayments start rose from £15,795 (2012 and RPI-linked) to £21,000 (2016 and earnings-linked thereafter). The rate of repayment is unchanged at 9% of the excess.

• Any outstanding debt is written off 30 years after the April following graduation, rather than 25 years.

The Institute for Fiscal Studies (IFS) had undertaken some new number-crunching on student finance to see what the long term effect of higher and more costly borrowing is likely to be. Its conclusions – which inevitably involve many assumptions – show that in many instances the line between a repayable loan and a non-repayable grant has become blurred:

• On average, students in the new system will graduate with debts of more than £44,000, over £19,000 more than under the old system.

• Whereas under the old system nearly half of students would have repaid their debt by age 40, only about 5% will have done so under the new system.

• The new system will see nearly three quarters of all graduates being left with outstanding loans to be written off, probably in their early 50s. The IFS thinks the average write off will be around £30,000.

If you have children or grandchildren at, or likely to go to university, the IFS numbers raise an interesting conundrum. Helping to meet fees or other costs covered by borrowing may simply mean that you are saving the government money because of the 30 year write off. On the other hand, the prolonged burden of debt repayment will leave most graduates still making repayments throughout their forties and, if they are higher rate taxpayers by then, facing an effective marginal rate of tax, national insurance and loan repayment of 51% on debt carrying interest at RPI+3%.

When saving for 10 years pays more than saving for 40

Apr 11, 2014

Which will give you a bigger pension: saving for 40 years or just 10?

Believe it or not, the answer is 10 – if those years are at the very beginning of your working life.

Someone who starts saving at the age of 21 and then stops at 30 will end up with a bigger pension pot than a saver who starts at 30 and puts money aside for the next 40 years until retiring at 70.

This astonishing outcome is entirely due to the power of compound interest – the way that investment returns themselves generate future gains. Having 10 extra years for compound interest to work its magic has the same result as all those years of extra contributions

The conclusion emerges from figures calculated by CLSA, a research company, and assumes investment growth of 7pc a year.

The company looked at savers who each contributed £2,500 a year to a pension.

The first, who started saving at 21 and stopped at 30, would have a pension fund worth £553,000 by the age of 70. This assumes that no further contributions were made but that the fund carried on growing at 7pc a year, with these gains reinvested in the pension.

The second saver, who starts at 31 and carries on contributing until the age of 70, ends up with a fund worth £534,000, again assuming 7pc annual growth.

The total contributions of the early-bird saver come to £25,000 and grow by a factor of 22. The late starter will pay a total of £100,000 into the fund and see his or her money grow a little more than fivefold.

A third scenario is perhaps even more startling.

Some parents begin a pension or other savings plan for children as soon as they are born, sometimes to benefit from the tax relief on up to £2,880 that is available to everyone, even babies. If your parents pay £2,500 a year into a pension for only the first two years of your life – a total of just £5,000 – and the money then remains invested, growing at 7pc a year with compound interest until you are 70, a fund worth £551,000 will be the result.

Another simple illustration of the unexpected effects of compound interest is to ask how long it takes to double your money if you make compounded returns of 10pc a year. The intuitive answer is “10 years” but it actually takes just seven. In fact, to double your money in 10 years requires a compound return of only 7pc a year.

Terry Smith, the manager of the Fundsmith Equity fund, which aims to invest in businesses that use the compounding effect on their own profits, pointed out the effect of a seemingly small improvement in returns on the final value of a savings plan if compound interest were allowed to work over a long period.

He asked: “Starting with £10,000, what is the difference in final capital from 30 years of investment at 10pc a year compound versus 30 years at 12.5pc a year ? The answer, rather surprisingly, is that the extra 2.5pc of compound return would double the final sum – so £10,000 invested would become £342,000 at 12.5pc as opposed to £175,000 at 10pc.”

Albert Einstein called compound interest the “eighth wonder of the world”, adding: “He who understands it earns it; he who doesn’t pays it.”

Darius McDermott of Chelsea Financial Services, the investment shop, said: “The lesson from all these figures is that there is no amount too small to start investing and that starting early gives you a huge advantage.

“But they also show how crucial it is to stay fully invested and to keep reinvesting any interest.” He said investors who pulled their money out in 2008 when the financial crisis began would have missed out on the rally in the markets over the six years since. “If you’re investing for the long term, it is important that you hold your nerve when the market is struggling and continue investing,” Mr McDermott said.

“It’s very hard to get rich quickly but it’s quite possible to get rich if you keep reinvesting and you have time on your side.”

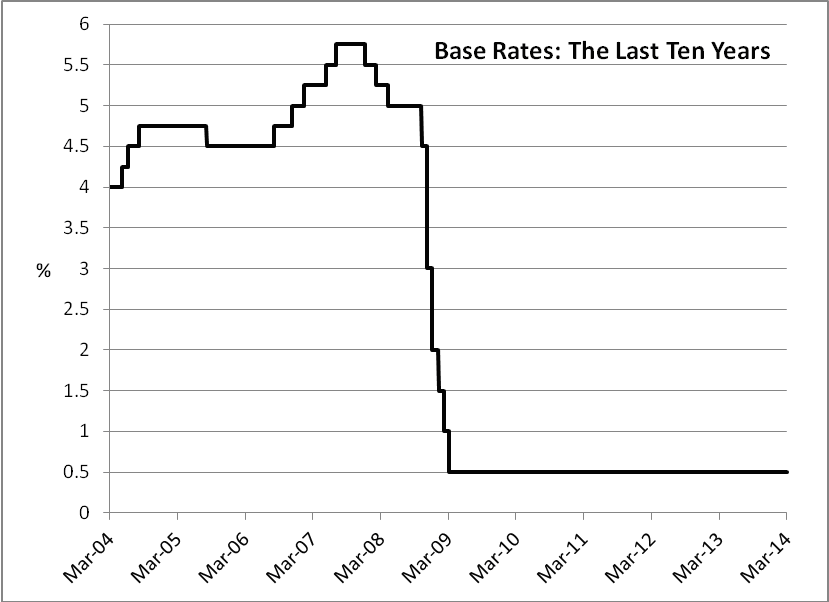

5 Years On....

Mar 7, 2014

The 0.5% base rate is celebrating its fifth anniversary this month, how long will those low rates continue.

On 5 March 2009 the Bank of England halved base rate, from 1% to 0.5%. As the graph shows, base rate had already been on a precipitous decline, having been 5.0% in October of the previous year. The move in March 2009 was an emergency measure at the height of the financial crisis: nobody was expecting that half a decade later base rate would still be at 0.5%.

The fact that 0.5% remains the choice of the Bank’s Monetary Policy Committee (MPC) can be linked to something else that until recently has been almost as static: the UK economy. Evenwith the near 2% growth experienced last year, the size of the UK economy remains more than 1% below the level it reached six years ago, in the first quarter of 2008.

The outlook for base rates was originally addressed last August by the then newly installed governor of the Bank of England, Mark Carney. His “forward guidance” was that base rate would only be reviewed when unemployment fell to 7.0%, which the MPC projected would be around mid-2016. That did not work out as expected and by January 2014 the unemployment reading was 7.1%, forcing the MPC and Mr Carney to rethink their guidance.

The result emerged alongside the Bank’s February quarterly inflation bulletin and, predictably, guidance is no longer tied to a single figure. Indeed, the Bank suggested that it would be monitoring a wide variety of economic factors to help it make future rate decisions. It also signalled that “if and when the time comes that the economy can sustain higher interest rates, Bank Rate is expected to rise only gradually.” The nearest Mr Carney came to making any forecast was to give an acquiescent nod in the direction of the market’s implied forecast for future base rates, “which approaches only 2% three years from now.”

Of course, a lot could happen in the next three years …or nothing, as in the last five.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Pensions - Tax Year End Planning

Feb 14, 2014

On 6 April 2014, two major changes will take effect to pension allowances:

- The Annual Allowance (AA), which effectively sets the maximum tax efficient pension contribution from all sources during a tax year, will be cut from £50,000 to £40,000. This is the second cut to the AA, which was £255,000 in 2010/11.

- The Lifetime Allowance (LTA), which effectively sets the maximum tax efficient total value of pension benefits, will be cut from £1.5m to £1.25m. This is also a second cut – the LTA was £1.8m in 2011/12.

The AA cut is a reminder of the importance now of taking full advantage of each year’s AA. When the allowance was £200,000+, regular contribution was a much less important factor. Fortunately, if you have not used the full AA in any of the three previous tax years, there is scope to do so using special “carry forward” provisions. 5 April (a Saturday) is the final day for carrying forward any unused AA from 2010/11.

As far as the LTA reduction is concerned, the government has announced two transitional protection options for those who are, or might in the future, be affected. One of these options, Fixed Protection 2014 (FP2014), will only be available to claim until 5 April 2014, while the other, which has more limited scope, will not be finalised until summer. Very broadly speaking, FP2014 will preserve your LTA at a minimum of £1.5m, provided that from 2014/15 onwards, no more contributions to your pensions are made and you accrue no further benefits.

If carry forward and/or the new transitional protection could be relevant to you, you should seek expert advice as soon as possible. Both are aspects of pensions which may involve considerable research before a decision can be taken.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.

Tax Year End Planning

Feb 14, 2014

The Budget is on March 19, so tax year end planning time has arrived.

Although the UK economy is now generally seen as firmly in recovery mode, the austerity regime of tax increases – disguised or otherwise – is continuing. Much as politicians will like to talk about tax cuts, a Budget deficit of around £110bn shouts more loudly.

Among the items to review on the investment front are:

- ISAs The maximum ISA investment in 2013/14 is £11,520, of which up to £5,760 may be in a cash ISA (probably earning interest below that 2% inflation rate). You cannot carry forward unused ISA allowances, so as far as possible you should contribute each tax year. The tax benefits of ISAs are well demonstrated by the fact that last year the Treasury examined the option of capping their value.

- Capital Gains Tax In 2013/14 you can realise gains of up to £10,900 with no capital gains tax liability. As the developed markets generally rose last year, you may find some gains in your portfolio that you can realise. You cannot simply sell and then immediately repurchase to crystallise a gain, but there are other options which have similar effect. For example you could sell your direct holding and then buy back in an ISA.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.

AVOIDANCE, TAX PLANNING AND FAIRNESS

Jan 31, 2014

HMRC is winning its battles against complex tax avoidance schemes…and it needs to.

The many pages of Treasury documentation issued in the wake of last month’s Autumn Statement included a ‘Scorecard’ listing the revenue impact of the Chancellor’s actions. Of the 59 items listed, 13 fell under the heading of “Avoidance, tax planning and fairness”, while another seven were captured by the grouping of “Fraud, error and debt”. Together the 20 measures listed are meant to raise an extra £1,515m for the Exchequer in 2014/15 and nearly £8,900m in total by the end of 2018/19.

That serves a reminder of the resources being given by HMRC to maximise taxpayer receipts. It is one of the inevitable consequences of a situation where further tax increases have become politically difficult. According to recent information obtained from HMRC, in 2012/13 £20.7bn in extra revenue was raised as a result of ‘compliance work’, up £2.1bn on the previous year and £2bn above its original target.

The Autumn Statement noted that since the Budget in March, the government had signed automatic tax information exchange agreements with the Isle of Man, Guernsey, Jersey, the Cayman Islands, Gibraltar, Bermuda, Montserrat, the Turks and Caicos Islands and the British Virgin Islands. In 2014 HMRC will start work “to exploit the data generated” by the new agreements. There was also a promise in the Autumn Statement that “At Budget 2014 HMRC will consult on a range of enhanced sanctions to penalise those who hide their money offshore and enhance deterrence.”

The irony is that the success of the UK in securing information exchange agreements is down to the US’s imposition of FATCA (Foreign Account Tax Compliance Act). This US legislation has given the HMRC considerable leverage with the Crown Dependencies, as each needed UK government consent for FACTA to operate.

Warm island homes for hot money are becoming scarcer by the day…

The Financial Services Authority does not regulate tax advice.

The Financial Services Authority does not regulate tax advice.

Better Be A Baby Boomer

Jan 24, 2014

Are you better off than your parents?

In an attempt to answer this question, the Institute for Fiscal Studies (IFS) has been looking at wealth for the generations born between the 1940s and 1970s. It has come up with some interesting findings:

- The lack of growth in incomes of working age households in the last 10 years means those born in the 1960s and 1970s have not seen the rapid rise in income between the ages of 30 and 50 that their predecessors (including the baby boomers) did.

- For much of their earlier adult life, the 1960s and 1970s groups did have higher take-home incomes than their predecessors enjoyed at the same age. However, this was matched by higher spending, with the result that the extra income did not generate any extra saving than the earlier generations achieved.

Those born in the 1960s and 1970s will find that their state pension (eventually) replaces a lower proportion of their income than for earlier generations, with the affect

- most noticeable at the higher end of the income scale. The cause is primarily the single-tier pension, due to arrive in 2016.

- It is taking longer to get on the housing ladder. 66% of those born between 1970 and 1976 owned a home at age 35, compared with 71% of those born in the 1950s and 1960s. In recent years, the homeownership rate among those born in the 1970s appears to have stalled at about two thirds. For the generation born in the 1940s and 1950s, the corresponding rate by the same age was 80%. The average age of second-time buyers has risen by 15 years (to 42) since the 1960s.

- The proportion of the younger groups who expect to receive an inheritance is far larger than the number in older groups who have done (or will do) so. 28% of those born in the early 1940s have received, or expect to receive, an inheritance against 70% of those born in the late 1970s. As the IFS says, “Inheritances look like the major potential reason why the later economic position of [groups] born in the 1960s and 1970s could yet turn out better than that of their predecessors, on average.”

So, if you are a baby boomer, for your children’s sake make sure your estate planning is up to date. If you are younger, start showing your parents some respect…

The Financial Services Authority does not regulate tax advice.